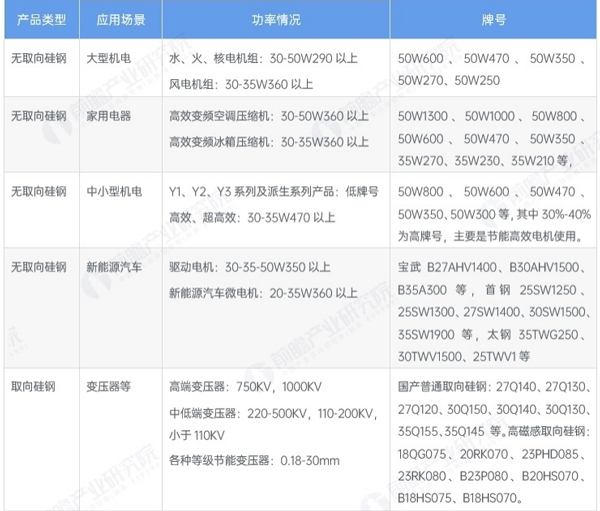

The downstream application areas of China’s silicon steel industry are primarily home appliances, small and medium-sized electromechanical equipment, new energy vehicles, large electromechanical equipment, and transformers. In terms of application, large electromechanical equipment, such as wind, thermal, and hydropower generation equipment, requires silicon steel for generator cores and other components to achieve efficient electromagnetic conversion and improve power generation efficiency. Non-oriented silicon steel is also required for motors in home appliances. Although the amount used per unit is relatively small, the large production volume makes the overall consumption significant. Air-conditioning compressor motors utilize a large amount of non-oriented silicon steel, especially with the increasing demand for high-grade non-oriented silicon steel as air conditioner energy efficiency upgrades occur. In the new energy vehicle sector, the demand for silicon steel in new energy vehicle drive motors is high. To improve motor performance and energy density, high-grade non-oriented silicon steel is generally used in the stator and rotor cores to ensure efficient operation across the entire speed range. In the industrial small and medium-sized electromechanical sector, motors used in rolling mills, cranes, and other equipment require silicon steel to power them to meet the high loads and high power requirements of metallurgical production processes. In transformers and converters, oriented silicon steel is primarily used in transformer cores. With the advancement of power grid construction, ultra-high voltage transmission projects, and the need to improve the energy efficiency of power transformers, the demand for high magnetic induction oriented silicon steel continues to grow.

Changes in the application scenario structure of silicon steel

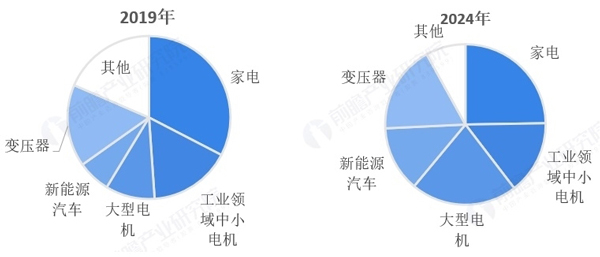

The main downstream applications of silicon steel in China include home appliances, large motors, small and medium-sized motors, and new energy vehicles. Based on these main applications, transformers and similar products almost exclusively use grain-oriented silicon steel; therefore, the usage proportion of transformers and similar products is equivalent to the proportion of grain-oriented silicon steel in the overall silicon steel production. In 2019, home appliances were the dominant demand sector for silicon steel, accounting for 40% of non-oriented silicon steel production and 33% of all silicon steel production. With slowing demand from home appliances, increased investment in large motors, and expanded production in new energy vehicles, demand from home appliances is being squeezed. Preliminary estimates suggest that by 2024, silicon steel demand in the home appliance sector will decrease to 25%, while in the industrial sector, small and medium-sized motors will account for 15%, large motors will increase to 21%, new energy vehicles will increase to 13%, and other sectors will account for 8%.

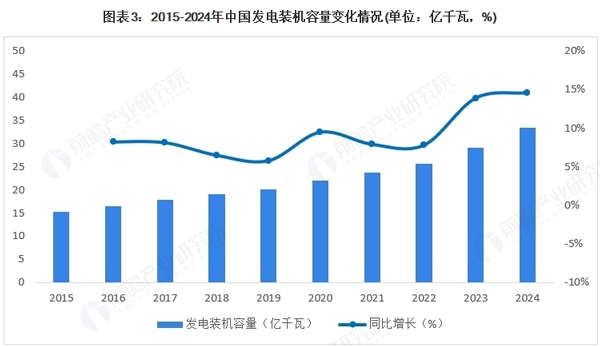

Power generation capacity climbs

Large-scale generators are primarily used in the power generation industry. Under my country’s overarching goals of “carbon peaking” and “carbon neutrality,” the driving force for power development is shifting from traditional coal-fired power to clean energy.

During the 13th Five-Year Plan period, the total installed power generation capacity nationwide grew at an average annual rate of 7.6%, with non-fossil energy capacity growing at an average annual rate of 13.1%. Its share of total installed capacity rose from 34.8% at the end of 2015 to 44.8% at the end of 2020, and coal-fired power capacity fell below 50% for the first time. From 2015 to 2024, China’s installed power generation capacity is projected to rapidly increase from 1.525 billion kilowatts to 3.35 billion kilowatt-hours, reflecting the strong growth demand in the power industry.

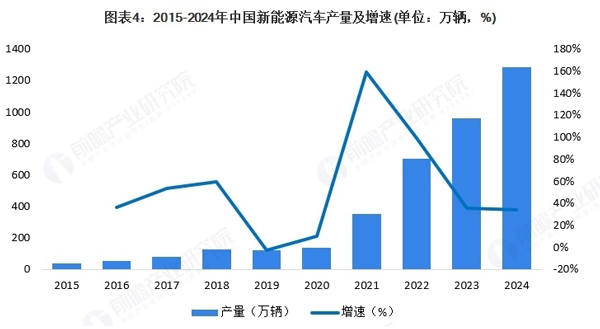

New energy vehicles boost demand

According to information released on the Chinese government website, my country currently ranks first in the world in the production of new energy vehicles. In terms of new energy power batteries, the “three-electric” technologies (battery, motor, and electronic control) have gradually established a competitive advantage. Intelligent cockpits and intelligent driving applications have reached international advanced levels. Significant progress has been made in power battery technology, with the energy density of mass-produced ternary lithium batteries reaching 300 Wh/kg. The performance of new energy vehicle drive motors has improved, with peak power density exceeding 10 kW/kg and maximum speed exceeding 20,000 rpm. 800V silicon carbide electric drives and 5C ultra-fast charging are rapidly becoming widespread, and the average energy consumption of pure electric passenger vehicles is approaching the planned target of 12 kWh/100km. The industry is in a stage of rapid development.

Starting in 2023, new energy vehicles will no longer receive subsidies, and vehicle production will slow down due to the impact of downstream demand. In 2023, China’s new energy vehicle production reached 9.587 million units, ranking first in the world. Production in 2024 is expected to reach 12.88 million units, a year-on-year increase of 34%.

Home appliances are mainly for renovation needs.

According to data from the China Household Electrical Appliances Industry Information Center, demand in the home appliance industry is sluggish. This is due to two main factors: firstly, fierce competition in online channels, with brands engaging in price wars that have squeezed profit margins; and secondly, the weak real estate market, which has impacted the home furnishing industry. In recent years, the home appliance industry has placed higher demands on energy efficiency management. For example, the successive releases of standards such as GB12021.2-2015 “Energy Consumption Limits and Energy Efficiency Grades for Household Refrigerators,” GB21455-2019 “Energy Efficiency Limits and Energy Efficiency Grades for Room Air Conditioners,” and GB18613-2020 “Energy Efficiency Limits and Energy Efficiency Grades for Electric Motors,” as well as the planned revision of GB30254-2013 “Energy Efficiency Limits and Energy Efficiency Grades for High-Voltage Three-Phase Squirrel-Cage Asynchronous Motors” in 2025, all impose higher energy efficiency requirements on refrigerators, air conditioners, and industrial motors. In 2023, my country’s cumulative air conditioner production reached 244.87 million units, a year-on-year increase of 13.5%; refrigerator production reached 96.323 million units, a year-on-year increase of 14.5%; and washing machine production reached 104.583 million units, a year-on-year increase of 19.3%, indicating a recovery in overall demand compared to 2022.

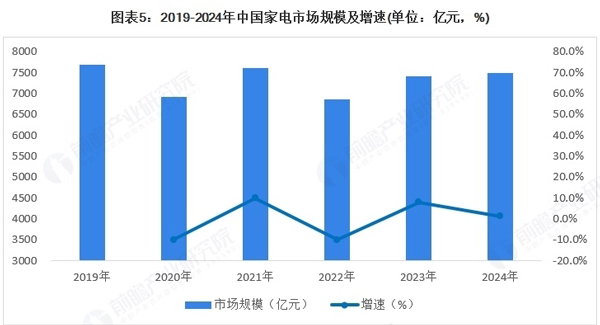

According to data from the China Household Electrical Appliances Industry Information Center, the size of China’s home appliance market fluctuated and declined from 769.5 billion yuan in 2019 to 740.5 billion yuan in 2023. The market size is projected to grow by 1.3% year-on-year in 2024, reaching 750 billion yuan.